First, tell me what is sold to us?

Remember, some CA, or a finance guy or nowadays any influencer (that too on reels) giving financial

independence tips and telling you the FIRE movement.

What is (FIRE)?----

Financial Independence, Retire Early (FIRE) means saving and investing around 70% of the income now so that

you can retire early.

According to FIRE, when that money after saving and investing every year reaches around 30 times the yearly

expenses then one can quit the day job or completely retire from any form of employment altogether.

Example:

If the yearly expenses are around Rs. 5 lakh with a moderate lifestyle,

then the money required for retiring is around Rs. 1.50 crore.

Okay! So now we understand what is sold to us.

But what is the problem with the FIRE movement, isn’t it a piece of great investment advice?

Let’s just break down the idea of the FIRE movement with an example.

Consider FIRE MODE ON till 35 years of age.

Monthly income: Rs. 25,000 (Most engineers monthly salary)

Saving and Investing: 70% which is 17,500.

Needs and Wants: 30% which is 7,500.

Challenges with FIRE:

- What about inflation and lifestyle inflation? Is it covered in the 30x.

- Practical challenges with allocations:

How can you sustain in a metropolitan city with Rs. 7500?

How can you tell that there would not be any emergency situation coming for the next 10–15 years?

There is no emergency fund allocated at all for any worst-case scenario…

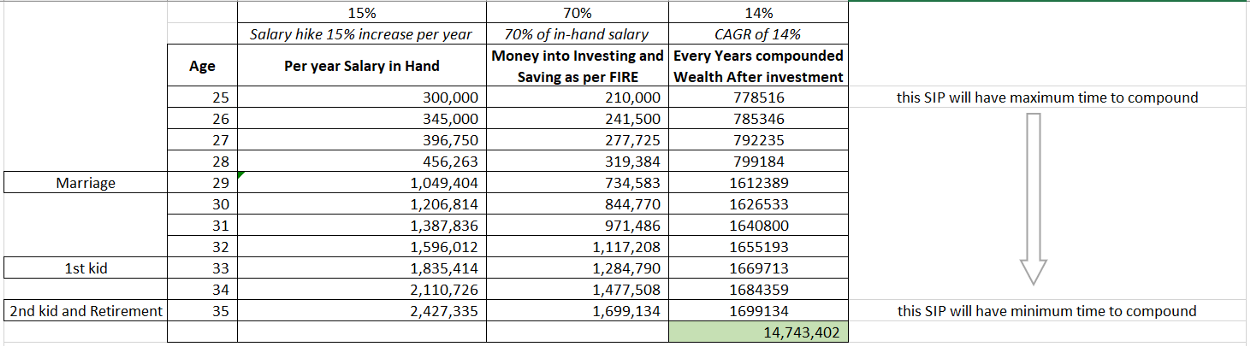

- Consider the below table:

As calculated earlier, the day you have 1.5 crores you are going to retire. So you take that money out

of the assets it was in and put it into a savings bank account. (Safety obviously)

So at the age of 35, you will have around 1.5 crores and 1 wife maybe and 2 kids.

Now, you not only have to worry for yourself but even for your kids' diapers, tutions, extra lectures,

game-skins, insurance, their Ivy Leagues and let us not forget world tours.

And yes! KIDS ARE EXPENSIVE.

Imagine 3 of them, Nightmare!

Imagine higher education costing around 50–60 lakhs per kid.

You have exhausted your 1.2 crores in a jiffy which you have been collecting for over 14 years.

- Also what happens to existing liabilities, EMI’s, Home or Personal loans, your own education breaks for

MBA, MS, Ph.D. from the age of 25 to 35.

- Once you retire you have to shift all your money into savings which cannot beat inflation at all

post-retirement.

What to do then?

What to do then?

There are two key factors that are important in achieving financial freedom:

-

Supply-side:

Ensuring that you’re acquiring assets that earn for you in the background.

- For acquiring those assets, start experimenting with different ways you can earn money at the

start of your corporate career since you have fewer responsibilities at home and work.

- Gain knowledge about tools like REIT, smallcase, Index Funds, SGB’s, etc. along with the

traditional Cryptocurrency, Mutual Funds and Stock Markets. (these have become traditional only

because ofThe Pandemic

Investors.)

- Demand-side:

Ensuring that your expenses are controlled and they don’t increase as your wealth increases.

Work hard and enjoy your life. Sometimes we might miss some moments in life when we don't

participate. Spend where it is required. Be frugal where it is meant to be. Love the process and

stay invested as we don’t know what the long term is until it is.

Investment advice varies as per individuals and cannot be generalized. There are a lot of factors

that cannot be predicted, not even by an economist.